I’ve been on an HSA+HDHP for a couple of years now and only realized recently the interest earned from investing HSA money is also tax free, so I want to start investing a part of my savings and see how it goes. I have 2 options, Betterment or Mutual Funds. I figured I’d try the latter to avoid fees, but I’m not sure which funds to choose. My HSA currently provides 30 fund options.

I see people mentioning Vanguard a lot so I spread out my initial investment into 25% chunks across 4 different Vanguard funds. How did I choose them? Well I literally just looked at the performance graphs and selected the ones that historically went up steadily without major dips. As a total noob, how can I improve my choices? Is there a simple way to decide without having to dive deep into the stock market?

A total market fund, or S&p 500 fund would be a good start. Pick something with a low percentage fee

100 percent this. Anything SP backed is gonna be safe. Unless you can do a CD, some have good rates of like 4-5 percent. T-bills tend to be too low yield for me tho.

Thanks! Noob question - what is a “low percentage fee” in this context?

It’s the fee the fund manager charges. Looking at mine, they call them expense ratios. Big broad stuff like S&p and total market is typically low fee <1%. But something that tracks a specific market sector, or a really active fund could charge >5%

Gotcha. Thank you for the explanation!

Just to emphasize the importance of low expense ratios: you don’t just lose the money you pay to the fund manager. Over time you also lose what that money could have made if it had stayed invested. Even a modest retirement fund can have an opportunity cost of $50k by the time you retire. As another commenter said, Vanguard tends to have the lowest fees.

Decimal fractions of a percent are low fee. Vanguard is mostly, if not completely, low fee.

To quantify it, anything under 0.20% is “low” to me, and many funds are <0.05%.

That said, once you get below a certain amount, comparing between “low” fees isn’t very interesting. For example, my 401k is switching their S&P 500 fund from a 0.04% fund to a 0.015% fund, which is >2.5x lower fees, but in terms of actual dollar amounts is pretty inconsequential (e.g. for $100k invested, it’s $25/year savings. At that point, I’m much more interested in the quality of the fund (i.e. how well it tracks its index) than the actual fees, since even a small amount of inefficiency (more cash, late rebalances, etc) can be much more impactful than that fee difference.

So anything under 0.50% is fine, and anything under 0.20% is “good,” and comparing expense ratios breaks down when the difference is <0.05%. At least that’s my take.

Go for whatever is the most diverse, without dipping too heavily in any one area.

Thanks. What does “diverse” mean in that context? I split it equally into 4 chunks, although all Vanguard. Do you mean I should also put it into non-Vanguard mutual funds like Schwab, etc.? Vanguard is like 10 of the 30 of my options to choose from.

You can have it all with one brokerage in one fund and still be diversified. Suggest reading up on the 3 fund portfolio or boggle head.

S&P 500 is top 500 US companies. Many folks consider that diverse. You can also probably find a US Total Market fund. That will be even more diverse as it will include small and mid size companies in addition to the top 500.

Alternatively, even more diverse would be a Total Market fund. These typically include international companies, and represent the biggest diversification you can get.

No need to worry about Vanguard versus Schwab . The underlying stocks of the fund is what matters.

Thank you! Your explanation clicked in my head. I thought Vanguard vs Schwab, etc. meant different underlying stocks; didn’t understand that’s the brokerage. I will definitely take everyone’s advice and look at the S&P 500 (I think that’s one of 4 I chose, I’m not at my desk right now).

Just to reiterate, having more funds doesn’t mean you’re more diversified. For example, let’s say you have the following (ETF/Mutual Fund tickers):

- VOO/VFIAX - Vanguard’s S&P 500 fund

- VTI/VTSAX - Vanguard’s Total US Market fund

- VV/VLCAX - Vanguard Large Cap CRSP fund

- VONE - Vanguard Russell 1000 ETF

These are all basically the same thing.

Let’s compare to just two funds:

- VTI/VTSAX - Vanguard Total US Market Fund

- VXUS/VTIAX - Vanguard International Total Market Fund

This is way more diversified because VXUS/VTIAX has a lot of stocks outside the US, so if the US tanks relative to the rest of the world, you’ll be better off. You can even make it just a single fund, VT/VTWAX, which gives you global exposure (something like 60/40 US/international).

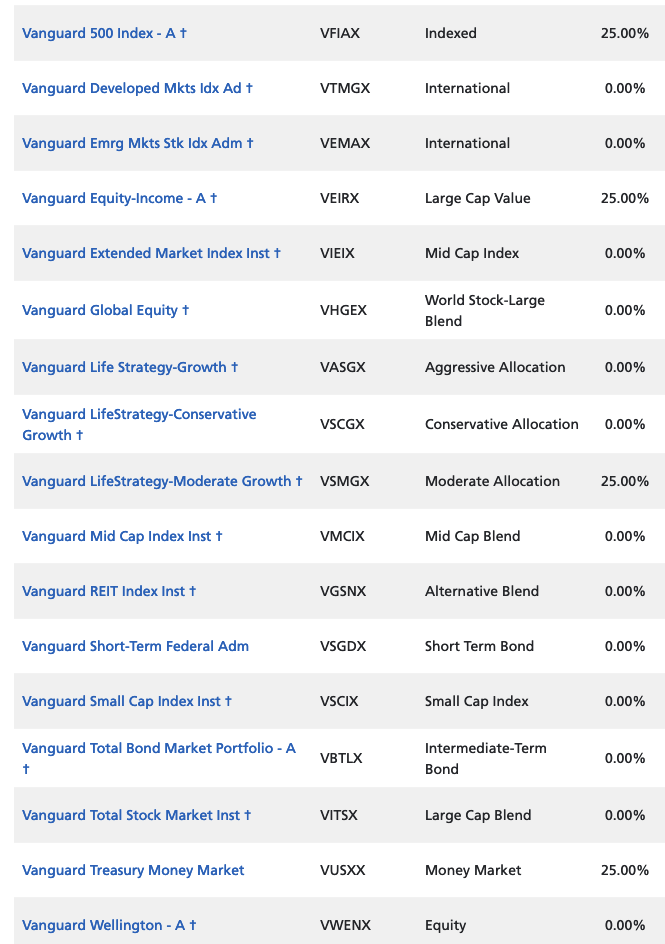

Thanks. Here’s a screenshot of my options:

https://files.catbox.moe/dezord.png

You can see where I randomly allocated each of the 25% of my investment. Is “Vanguard 500 Index - A” the same as the S&P fund that everyone is recommending? And should I just move everything there instead? I’m guessing I need to choose one of the 2nd and 3rd in the list for the international side so I’m not overly dependent on the US market?

Yup, VFIAX (the Vanguard S&P 500 index) is what everyone is saying.

Here’s what you’re invested in:

- VFIAX - S&P 500 fund; 500 biggest companies in the US

- VEIRX - basically a “value” tilt version of the S&P 500, but with far fewer companies (~200 vs 500)

- VSMGX - conservative, properly diversified fund - 60% in stocks (diversified with international stocks), 40% in bonds

- VUSXX - basically cash

So overall, here’s what you’re looking at (back of the napkin math):

- 35% - cash and bonds

- 55-60% - US stocks

- 5-10% - international stocks

So you’re pretty lightweight on international stocks.

Personally, here’s what I’d invest in:

- VITSX - Total US market, meaning there are smaller companies in there as well; 85% of it is the same as the S&P 500, so it’s not that different, but small companies have historically done better than big companies, so it’s good to have some of that exposure

- VTMGX - pretty much total international market

To be evenly diversified globally, you’d do something like 60% VITSX and 40% VTMGX, but I personally think the US will outperform, so I do 70% US and 30% international.

If you’re risk-averse and feel like you’d sell if there’s a market downturn, you can add some bonds (VBTLX) and put something like 10-20% in it (assuming you’re young-ish; if you’re over 50, increase it to 30-40%). But honestly, there’s not much point if you’ll just set it and forget it. If you want something super simple, VASGX looks pretty decent (20% bonds, so a bit less extreme fluctuations in a downturn).

A lot of people honestly just go 100% S&P 500, because a lot of those companies do business in other countries, so you’re kind of getting international exposure. I personally prefer explicit international exposure though, hence my recommendation.

Thank you so much for the very detailed information! This is honestly the best direct advice I’ve gotten that is understandable for someone like me who knows nothing about it. I will use this info as a starting point and re-allocate my funds accordingly.

I mean among positions. If you have 50% apple, 50% nvidia, you only have 2 stocks. Mutual funds are different baskets of stocks, but they can overlap, ie a US and a World Total fund would be doubled up on US.

I focus on market-cap weighted total world funds. I have 2 ETFs, VT and BNDW, and yet am the most diversified possible.

I’m lazy and went VWCE. A world wide index fund with exposure to US, EU, and Asian markets.

I buy a bunch every year, I don’t care about the buy price because the fund follows the market. If I get a few less because I got it on a rally, meh. If I get more because I got it during a dip, neat.

I joined https://www.bogleheads.org/ which was also when I started learning about mutual funds

Bogle started the first index fund family (Vanguard), so there is an index fund bias with many there, but the forum has very knowledgeable people. (Full disclosure, I am busy, and use indexing myself, but not in Vanguard.)

You have managed to hit the best all-around choices on your first try.

The large difference is to learn to have the discipline to ride out the ups and downs of investing. In a recession, it is a gut punch to see your hard-earned investments drop. The losing segment says the whole market is rigged, screw this and lock in their losses by selling. When the market improves, highs are being clocked, these same are likely to forget their previous folly and buy in again. It is investing that is controlled by emotions, and is a buy high, sell low outcome. Mastering your emotions in investing is the key to investing. Many people give 1/4th of their money to brokers so that they will be reminded of the previous paragraph, when they need it most.

We are financially independent thanks to indexing, and using emotions in a constructive way. We also have been through a few ups and downturns, making money in each cycle, by riding it out, and asset allocation.

Follow your plan and ride things out, and you will likely be a multi-millionaire. It is not overnight, though.

schwab has an autobalancing option for a mix of stocks, bonds, and if you set it aggressive even commodoties I think. then there are at least I think two mutual funds that autobalance stocks and bonds and I think vanguard has one of them but you will have to look them up as a quick search did not get it for me and I don’t feel like going further. but its a thing that exists.

We’d really need to know what the 30 options are, to recommend one.

But I’d really recomend against it. The point of an HSA is to have cash available for medical expenses and emergencies. Over the long term (decades) index funds do consistently trend up. But on any given day, you never know. Money you were expecting to be there might not be. Now you’ve got a whole other problem.

If you have more money than you can imagine needing in the HSA, pick something with slow consistent growth and low or zero volatility.

Thanks for the advice. Yup, I realize health funds shouldn’t be gambled, that’s why I’m taking a conservative approach and just investing a small % of my HSA. I’m at a point right now where I have enough funds for current health needs and emergencies (my current HDHP coverage is pretty good), so I’m just dipping my toes with increasing those funds via other avenues.

And for the 30 options, I’ll post back here when I get back to my desk.

- Low cost

- Broad base

- Index fund

The only three things you need to know about index investing.

The largest cost factor you can control is costs so if you want to improve your selection look for funds that have very low fees (I.e. <1%)

This fund will literally beat the vast majority of actively managed funds over 10 years.

Don’t believe me though, just read ‘The Bet’ section in the 2016 Berkshire Hathaway letter to shareholders.

If you have the time, read The Little Book of Common Sense Investing by Bogle. It will explain the principles most commenters are espousing here.

{kind=link}